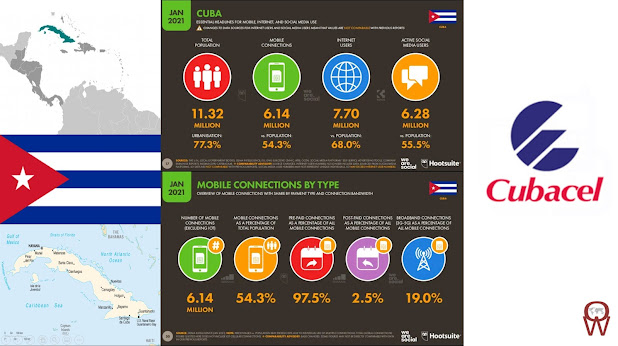

Cuba’s telecom sector is a unique one with state control having stymied rather than promoted the development of all sectors. The country has the lowest mobile phone and internet penetration rates in the region, while fixed-line teledensity is also very low. Fixed-line and mobile services remain a monopoly of the government-controlled Empresa de Telecomunicaciones de Cuba (ETESCA Cubacel).

Although there are still state restrictions over the right to own and use certain communications services, a thawing of relations between the US and Cuba has encouraged the government to improve access to services. Since 2015 Wi-Fi hotspots have been put in a number of places and since 2019, Cuba's Ministry of Communications (Mincom) has allowed individuals to create small private not-for-profit Wi-Fi networks and to import equipment.

Access to sites is also tightly controlled and censored. A DSL service was launched in March 2017 in areas of Havana and has since been expanded though costs have been set too high for most Cubans able to access the service. However, in 2019 Google and ETECSA signed an agreement to improve access for Cuba’s internet users by setting up a cost-free and direct connection between their respective networks.

Similarly, LTE services have been launched, with over 473 LTE base stations having been built across the island by the end of 2019. The mobile user base has grown to over six million, 70% of which are smartphone users.

Many consider Cubacel the only mobile provider in Cuba as the other C-com stays invisible. Cubacel started with a TDMA-network on 800 MHz which was decommissioned in 2009.

It's GSM-based network on 900 MHz nationwide for 2G with additional spectrum on 850 MHz in La Habana (= Havana), Varadero, Ciego de Ávila, Cayo Coco, Cayo Guillermo and Holguín (at the airport and Guardalavaca).

In 2017 Cuba’s state-owned telecoms operator ETECSA has announced that its customers are from now on able to send text messages to any mobile phone in the US and anywhere else. The cost is CUC 0.60 (US$ 0.60), with ETECSA stating that the charge is "similar to other international destinations".

In 2018 about 789 3G stations on 900 and 2100 MHz covered about 68% of the population and in 2019 this has grown to 85% of the population. The company intends to continue focusing on capacity expansion with a view to reducing prices and adding more users, although accessing mobile devices is a problem due to the ongoing US embargo.

In 2018 ETECSA also started to deploy 4G/LTE on 1800 MHz (B3). The operator has begun trials of 4G technology in northern Havana and in tourist hubs like Varadero, Cardenas, Mariel and Bauta. This trial 4G service is currently only available to some roaming customers and selected high-usage customers who consume over 1.5 GB of data a month, have compatible handsets and spend ‘significant amounts of time’ in coverage areas. ETECSA is aiming to bring 4G mobile services to all of the country’s 15 provincial capitals by the end of 2019.

In 2019 ETECSA has also unveiled new 4G/LTE mobile packages for prepaid customers, at the same time revealing that 3 million of its wireless lines were accessing mobile data services, following the commercial launch of 3G in December last year. The operator’s LTE network, meanwhile, was activated in the first half of 2019, but was initially restricted to selected high-usage customers. This service was opened up to prepaid users in October in the provinces of Havana, Matanzas, Mayabeque, Artemisa, Camaguey, Ciego de Avila, Holguin, Granma, Las Tunas, Guantanamo and Santiago de Cuba.

ETECSA has installed a total of 3,268 mobile base stations across the island, of which 1,357 are 2G, 1,438 3G and 473 are 4G base stations. The LTE total is expected to reach 500 by year-end, located in all provinces except Cienfuegos, which will be upgraded to enable 4G access next year.

Some 4.4 million Cubans used mobile internet services in 2020, while the number of cell phone users rose to 6.6 million, according to officials from the ETECSA.

Cyta for CYprus Telecommunication Authority is jointly owned by the Government of the Republic of Cyprus and Vodafone and is still the largest operator in the country giving a reasonable coverage at the highest rates around.

Cyta launched the first 5G network in Cyprus in January 2021.The Cytamobile-Vodafone 5G network has a population coverage of 70 per cent and is expected to reach 98 per cent in around 12 months, the company said. All Cytamobile-Vodafone subscribers, individuals and companies have access to the 5G network at no extra charge. All a subscriber needs is to be to have a 5G device certified on the Cyta network and to be in an area with 5G coverage.

At the 5G Techritory Conference 2021, Chrysis Phiniotis, CTIO of CYTA presented a talk on 'CYTA 5G Journey to the Top'. His talk is embedded below:

Back in October, Ookla®, the Speedtest® company, announced that Cyta had the fastest mobile network in Europe.

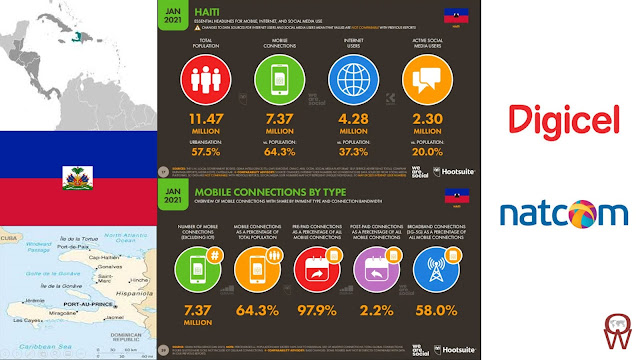

Haiti is the poorest country in the Western Hemisphere. Their economic and social indicators remain far lower than the average for Latin America and the Caribbean. The recent years of political and economic turmoil and natural disasters, including periodic and damaging hurricanes, have stifled most sectors of the economy, including the telecoms sector which remains one of the least developed in the world. In the internet market, poor fixed-line infrastructure has obliged most businesses to rely on satellite and wireless technologies.

Haiti currently has two mobile networks operaters: Digicel Haiti and Natcom.

Digicel came to Haiti in 2006 and has won the most customers since. The other provider Natcom was created after the privatization of the national operator in 2010 with Vietnamese help. Other networks often saw suspensions too: Concel sold its cellular network branded as Voilá to Digicel in 2012. The CDMA mobile network of Haitel was shut down in 2013.

In 2020 both operators were given a one year period of exclusivity in the provision of LTE services, though both had asked for four years. Their efforts in promoting LTE as well as innovative mobile data services such as mobile banking are going some way to improving internet connectivity in rural areas, and in coming years this will enable communities to make greater use of internet services in those many areas where fixed-line infrastructure remains inadequate.

However the mobile networks are unreliable and only cover some areas with 3G, often dubbed as "4G". 4G/LTE has started with Natcom. Many locals have two SIM cards, because of the situation as starter prices are minimal. WhatsApp is very popular to communicate.

Digicel has become the market leader with almost 3/4 of all mobile users in the country since its launch in 2006. It has a reasonable coverage for voice, but only some areas are covered by 3G for faster data which are marketed as "4G". These areas are shaded in dark red on this coverage map. 3G coverage is verified in Cotes des Arcadins, Anse A Galets, Saint-Marc, Gonaives, Cap-Haitian, Port-de-Paix, Hinche, Mirebalais.

2G/GSM up to EDGE is on 900 MHz and 1800 MHz and 3G labeled "4G" up to HSPA+ on 2100 MHz.

In October 2021 Digicel Haiti confirmed that 15% of its cell sites are currently unable to function due to ongoing fuel shortages and other issues around security. Digicel Haiti has around 1500 cell sites across the country. They confirmed that around 10% of these were non-operational due to a lack of fuel, demonstrating the scale of the escalation.

The outage has affected 200,000 mainly rural users of the company's services. Digicel has approximately 4.5 million customers in Haiti.

Natcom was created in 2010 after the privatization of the state-owned national provider Teleco with Vietnamese assistance. It's a joint venture owned 60% by Viettel and the Vietnamese army and 40% by the Haitian state.

The operators 2G is on 900 MHz and its 3G on 2100 MHz. 4G/LTE is on 1700 MHz (AWS, band 4). They hold a temporary 4G/LTE concession covering six metropolitan areas of the capital Port-au-Prince: Delmas, Petionville, City Centre, Carrefour, Tabarre and Plaine du Cul-de-sac. In 2018 finally the Haitian regulator CONATEL granted them bandwidth for 4G/LTE on 1700 MHz (band 4).

Natcom has still less coverage than Digicel, but offers in certain areas faster speeds and generally lower rates thanks to many promotions.

Natcom has built a 6,500km fibre backbone, which is helping to support growth in the fixed-line broadband sector, practical challenges mean that for the majority of people and businesses connectivity is achieved through mobile networks.

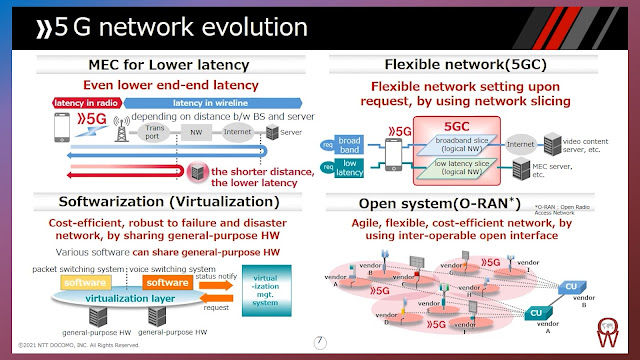

We have highlighted many firsts of Japanese operator NTT Docomo in many different posts in our blogs. For the regular readers of our blogs, it won't come as a surprise that NTT Docomo announced that they have already 10,000+ base stations based on O-RAN principles and the number is expected to exceed 20,000 by March 2022.

In fact NTT Docomo is also trying to export their know-how, partners and ecosystem to other interested operators. To highlight how this would work, they had also published a 5G Open RAN Ecosystem (OREC) Whitepaper back in June as can be seen in the Tweet above.

In not just the RAN virtualization where Docomo leads. Back in 2016, Docomo introduced world's first multi-vendor network virtualization technology to LTE packet service. By March, the core network virtualization adoption rate had increased to 56%. It is expected to reach the 100% target by the end of FY 2024.

At 5G Techritory conference, Takehiro Nakamura, SVP and GM of 6G-IOWN Promotion Department at NTT Docomo Inc., presented the 5G Status in Japan, most with regards to NTT Docomo. His talk contained some interesting nuggets and is embedded below, for as long as the talk is available online.

In addition, please check out all the posts below providing interesting insights from NTT Docomo.

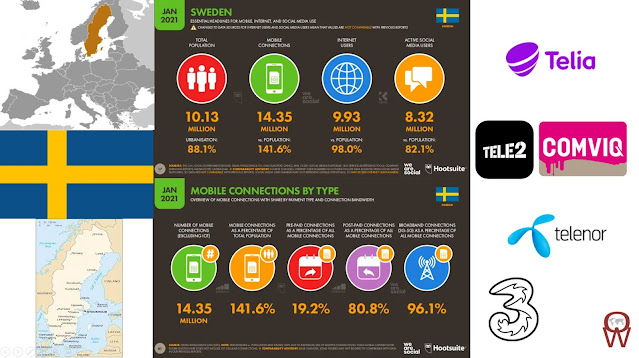

Sweden’s telecom market includes mature mobile and broadband sectors have been greatly stimulated by the progressive investment of the main MNOs in developing new technologies. The country retains one of the best developed LTE infrastructures in the region, while its MNOs have benefited from the January 2021 auction of spectrum in the 3.5GHz band which will enable them to expand services nationally.

Sweden has 4 physical network operators: Telia, Tele2 using brand name Comviq, Telenor (formerly Vodafone Sweden) and 3 (Tre).

However, all the 4 physical networks share 2G, 3G, 4G and 5G with at least one other network:

Telia runs its own 2G and 4G LTE networks. Its 3G network on 2100 MHz is shared with Tele2, while it has an own 3G network on the 900 MHz band.

Tele2 operates all its networks in cooperation with other operators: Tele2's 2G and 4G are shared with Telenor, while its 3G is shared with Telia.

Telenor's 2G and 4G networks are shared with Tele2, 3G is shared with 3 outside Stockholm, Gothenborg, Malmö, Lund and Karlskrona, where they have their own.

3 is the only Swedish network without any 2G. They currently have two different 3G networks, one on the 2100 MHz band, shared with Telenor (except in the cities named above), and one on the 900 MHz band, that they don't share. They have also built their own 4G network.

In 2021 Telia is market leader with the best coverage and 36% of customers, followed by Tele2 with 27% and Telenor with 19% and 3 with 15% in last position.

2G is on 900 and 1800 MHz like everywhere in Europe, 3G is on 900 and 2100 MHz. Tre does not have a 2G network.

All major 4 Swedish operators support 4G/LTE. Tele2 and Telenor have a joint LTE network called Net4Mobility claiming 99.5% coverage. LTE is on all carriers on 2600 MHz (band 7) in the cities. 800 MHz (band 20), 900 MHz (band 8, only on Net4Mobility) and 1800 MHz (band 3) frequencies are used additionally. Tre offers TDD-LTE on 2600 MHz (band 38) and FDD-LTE on 2100 MHz (band 1) in some locations. From 2019 700 MHz (Band 28) will be added by Telia and Net4Mobility.

Here's a beautiful collage of the 5G coverage maps of the *best covering* 5G networks per Nordic country: @TDCNET_DK, @ElisaOyj, @telianorge and @3Sverige. Yes, '3' has the widest 5G area coverage in Sweden - it says something about just how behind Swedish 5G rollout is. pic.twitter.com/bI1eKeU6C4

5G started to be available in Sweden during 2020 on some postpaid subscriptions on the four big operators and since September 2021 on some high-data Comviq postpaid plans, though not on prepaid and MVNO yet. Physically, 3 different 5G networks are being built: Telia and Tre will build their own networks, while Tele2 and Telenor continuing with their joint network Net4Mobility. Frequencies on 700 MHz (n28), 2300 MHz (n40) and 3500 MHz (n78) were auctioned to 4 providers in 2018 and 2021.

Both 2G and 3G are being phased out and are planned to terminated by 2025. Telia has announced that it will shutdown it's 2G network by 2025, but has started with its phase out. Telia has also said that it's own 3G network will shut down at the latest 2025, but it will dismantle individual sites as time goes. Tele2 has said that it's shared 3G network (that has been built with Telia) is being phased out since 2021 and will be completed at the latest 2025. So for data you need to have a device for 4G/LTE on the frequencies mentioned above, while a basic service will be maintained on 2G and 3G up to 2025 for voice and SMS services.

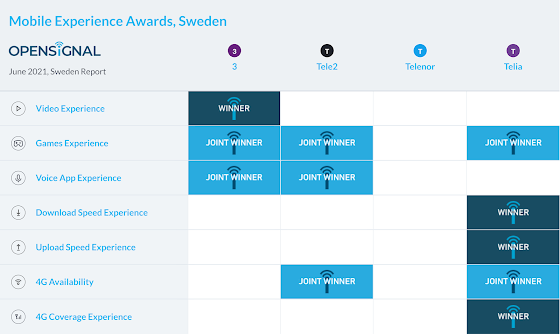

The OpenSignal June 2021 report on Sweden reveals a varied picture with three of the four national operators winning — or sharing the win — in at least three of the seven mobile experience categories. Telia solely wins Download Speed Experience, Upload Speed Experience and 4G Coverage Experience, while sharing the victory in Games Experience and 4G Availability. 3 leads in Video Experience and jointly wins Games Experience and Voice App Experience. Tele2 is a joint winner in Games Experience, Voice App Experience and 4G Availability.

Telia, owned by the Swedish Telia Company is market leader in Sweden with the best coverage nationwide in 2G, 3G, 4G and (on 800, 1800 and 2600 MHz): 4G/LTE is available for all prepaid products with up to 100 Mbit/s speed.

If one is visiting northern Sweden and intending to stay out of cities, then Telia or its subbrand Halebop will probably be the only network that has coverage.

In May 2020, Telia launched Sweden's first large-scale public 5G network in Stockholm. 5G is now being rolled out at a high pace from Skåne to Lappland and is already available in 22 cities. And in doing so, Telia managed to beat the Swedish 5G speed record. Telia collaborating with Ericsson means that 5G will have the same coverage as today's 4G network, in the period leading up to 2025 (covering 90 percent of Sweden’s geography and more than 99 percent of the population). As early as 2023, the 5G network will cover more than 90% of the population. 4G capacity will also double as part of the mobile network modernization. Telia’s 5G network uses higher frequency bands, such as 3.5 GHz, in densely populated areas with a lot of connected people and things using the network. The higher frequency bands are also used to build local, dedicated 5G networks for e.g., industry, ports, and hospitals. The lower frequency bands, such as 700 MHz, are used in rural areas to be able to offer good coverage and connection.

Comviq is a subsidiary of Tele2 in Sweden. That's why it uses the Tele2 and Telenor network on 2G, the Tele2 and Telia networks on 3G and Net4Mobility (= Tele2 and Telenor) on 4G with up to 80 Mbps speed. In September 2021, 5G on Net4Mobility was opened up to some high-data Comviq postpaid plans with up to 100 Mbps speed, but is not open for prepaid yet.

Tele2 doesn't sell own prepaid SIMs anymore, they are geared to contract customers and channel all prepaid products through their Comviq brand. They have a 99+% coverage on 2G, 3G and 4G/LTE.

Tele2 said it had switched on its commercial 5G network on May 24 2020. The operator said that the company’s customers will be able to enjoy the next generation mobile network in Stockholm, Gothenburg and Malmö. 5G services will be offered using 80 megahertz bandwidth on C-Band spectrum.

Telenor has a good 2G, 3G and 4G/LTE network up to 450 Mbps is available on Net4Moblity for prepaid too.

Telenor Sweden activated its 5G network in October 2020 in central Stockholm, marking the launch of nationwide roll-out using the new technology. The operator said the 5G network will provide internet access at 1 Gbps to customers with a compatible handset and a Telenor 5G-ready 30 GB, 75 GB or Unlimited subscription. The Telenor network uses 80 megahertz of spectrum in the 3.7 GHz band, which is shared with Tele2 via their Net4Mobility joint venture.

The next cities to get 5G will be Gothenburg and Malmö, and then the new network technology will reach cities with over 50,000 inhabitants, and finally, smaller towns. Telenor also said that it expects its 5G network to cover 99% of Sweden’s population by 2023.

3 (called "Tre") in Sweden has good speeds in 3G (on 900 and 2100 MHz) and 4G/LTE on (800, 2100 and 2600 MHz, partly as TD-LTE on band 38): Tre 3G and 4G coverage. Have in mind that Tre doesn't operate a 2G network and has no 2G roaming. You'll need to have a 3G or 4G device for using the Tre network. International roaming is blocked for all prepaid lines, you will be able to use their SIMs in Sweden only.

Tre Sweden (3 Sweden) officially launched its 5G network in June 2020 in Malmö, Helsingborg, Lund, Västerås, Uppsala and large parts of Stockholm. In December 2019, the Operator was the first in Sweden to launch a trial 5G network - then in southern Stockholm.

With nearly 400 active 5G masts, half of them in Stockholm, Tre said that it now has Sweden's most developed 5G network. The 5G network is activated using Tres' existing frequency spectrum.

All private customers with a 3Surf subscription from Tre and a 3G mobile from Tre, can access to the new 5G network at no extra cost. The same applies to corporate customers who have subscribed after January 15, 2019.

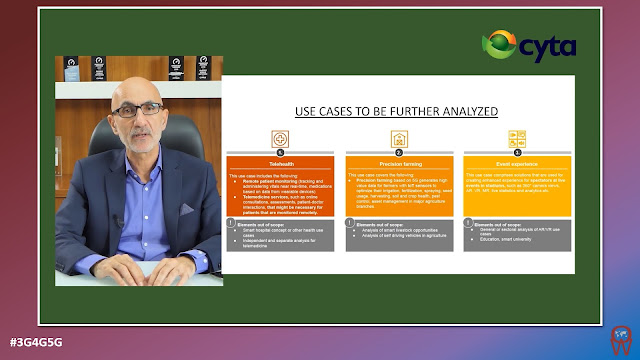

Since the launch of the first European 5G Standalone Network, Vodafone Germany has continued innovating, to find the killer use case. Here are some of them that they have been working on this year.

First 5G Hospital: In the first 5G clinic in Europe, the network of the future will make innovative applications possible in the future that will significantly improve the medical treatment and care of patients. Whether in surgery, in the emergency room or even when calling the emergency services: "Digitization can save lives", says Vodafone Germany boss Hannes Ametsreiter. In order to expand the digital possibilities in hospitals, the Düsseldorf network pioneer is now equipping the Düsseldorf University Hospital (UKD) with 5G power. "We bring our real-time network directly to the hospital to support patients and doctors with new technologies."

5G Telemedicine: State-of-the-art technology, sensors and a direct line to a doctor await you when you visit the doctor in the telemedicine station. The US company Onmed has now launched one of the first treatment rooms for remote treatment on the market. Go in, get treatment, get medication, go out again. A visit to the doctor in the telemedicine station could be so easy. The first Onmed stations are to be set up in the USA and worldwide this year. And now let's take a look. This is what you can expect when you visit the doctor in the telemedicine station

Research on the 5G train: Vodafone builds campus network for test track in the Ore Mountains - Imagine you take the train from Hamburg to Berlin - and that completely without a train driver: in. How this can work is researched and tested by Vodafone in cooperation with the Technical University of Chemnitz. With 5G and the Internet of Things, the two partners want to digitalize rail traffic sustainably in order to make it safer and more efficient.

Sky 5G Multiview App: Anyone watching football matches in the stadium wants to see top sporting performance on the pitch and experience pure emotions. But fans in the stands do not always get every detail of the game and miss some crucial scenes. 5G technology from Vodafone and the Sky 5G Multiview app could soon change that. The Sky 5G Multiview app combines the advantages of a live sports broadcast on home TV with real emotions in the stadium. Because the new app provides fans in the audience with exclusive content and makes it possible to experience the top game directly on the smartphone from five camera perspectives.

Football live with DAZN: GIGA 5G from Vodafone kicks off the real-time broadcast - Vodafone and the sports platform DAZN want to make live sports broadcasting with 5G technology more environmentally friendly, more efficient and more flexible. The two partners are working on a sustainable football live stream that brings the impressions and emotions from the pitch to your home in real time. Live broadcasts at sports events usually work like this: Several cameras are connected to an OB van via cables. From there, the recordings are forwarded to a broadcasting center via satellite and played out from there. All of this requires a lot of technical and human resources. The data exchange via the 5G network from Vodafone can simplify these processes considerably. With the innovative solution from Vodafone and DAZN, the camera is simply connected to a 5G-capable router and the recordings are transmitted directly to the broadcast center. No annoying cables, no OB vans and almost no delay.

Please note: All news item from German has been translated to English automatically using Google translate.

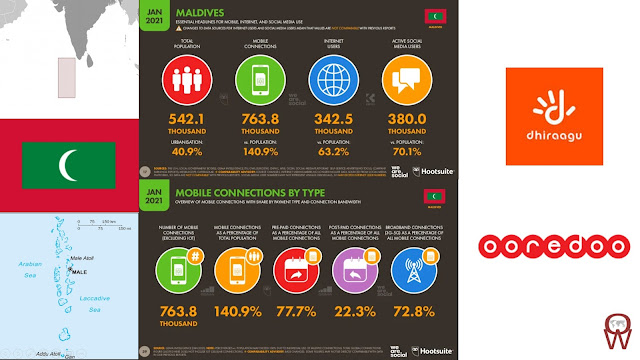

The telecom sector in the Maldives generates a limited revenue due to the relatively small local population, although the considerable influx of tourists increases this. The vibrant tourist sector helps to account for the unusually high mobile penetration rate, though multiple SIM card use is also widely adopted. In, addition a large number of expatriate workers require SIM cards on a semi-temporary basis. Steady growth in recent years has attracted international investment, including the Qatar-based Ooredoo Group.

The two licensed operators, Dhivehi Raajjeyge Gulhun (Dhiraagu) and Ooredoo Maldives, have both invested in HSPA and LTE infrastructure, providing national coverage with both technologies following substantial investment. This development has encouraged the take-up of mobile broadband services among subscribers. In late 2018 Dhiraagu trialled 5G technology, though commercial services have not yet been considered given the existing capabilities of LTE.

Both Dhiraagu and Ooredoo Maldives also provide fixed-line services and have greatly expanded the reach of their respective fibre networks.

The country has given priority to telecom infrastructure upgrades, with considerable success. There is a well-developed national network, and in recent years investment has been extended to outlying islands, following a period when commercial considerations focussed such investment in the capital Malé as well as in tourist resorts.

The submarine cable connection to Sri Lanka improved international bandwidth and helped reduce access pricing for end-users. A second submarine cable linked the archipelago to India in 2006. Additional cables linking the main atolls has substantially strengthened domestic connectivity

The two network operators: 2G/GSM is on 900 MHz, 3G on 2100 MHz up to (DC-)HSPA+ speed, 4G/LTE has started in 2013 on both providers on 1800 MHz (3) and added by 2100 (1) and 2600 (7) MHz. 5G started on Dhiraagu in Male in 2019 and is available without surcharge. Both networks have shops next door to each other at Male international airport.

Dhiraagu is the leading and the largest provider of telecommunications and digital services in the Maldives. It's mostly owned by the Batelco Group from Bahrain and the Government of the Maldives. They have linked the Maldives from north to south through a 1,253 km long fibre optic submarine cable network which supports the nation's largest 3G and 4G/LTE and fixed broadband networks.

4G/LTE started in Male on 1800 MHz (band 3) frequency band and has been expanded in 2015 to a few more islands and the 2600 MHz (band 7). In 2016 they completed a campaign to provide 3G services to 100% of Maldivians on all inhabited islands, and its focus is now on offering nationwide coverage of its 4G/LTE network, which is currently available to 60% of the population. Dhiraagu is aiming to complete the 4G/LTEexpansion project by the end of 2017

Dhiraagu made a huge fuss when it launched a commercial 5G service in 2019, but this service was basically only available to tourists with the correct phones.

Ooredoo was taken over and rebranded 2012 from Wataniya. It's the second mobile provider in the Maldives. LTE has started 2014 on 2600 MHz (band 7) in Male, now available to prepaid customers to be added by 2100 MHz (band 1).

Their coverage is good but not as good as Dhiraagu's. In 2017 LTE coverage has spread to 40 inhabited and resort islands, covering 75% of the population.

Ooredoo has launched commercial 5G services in the Maldives, with the initial rollout covering a large percentage of the capital city of Malé, including key business hubs, hospitals and public spaces. Ooredoo Maldives has also announced the simultaneous launch of 5G AirFibre, the Maldives’ first 5G-powered home broadband service.

At the GSMA Mobile 360 APAC – 5G Industry Community Summit, October 2021, Dr. Supakorn Siddhichai, Executive VP, Digital Economy Promotion Agency (DEPA) presented a Keynote looking at Thailand’s digital economy development plan, 5G City whitepaper, network and industry standards. His talk is embedded below:

Last week operators True and Dtac announced an $8.6 billion plan to merge. If approved by regulators, the new company would become the largest Thai telco by market share, accounting for about 54 percent of all mobile users. It would also effectively slim Thailand’s three-horse telco race down to a duopoly.

Thailand’s telecom market, with an estimated 91 million mobile customers, has for several years been a three-horse race. The industry leader is AIS, which has 46 percent of the mobile market and posts consistently strong earnings. In 2020 AIS reported 85.6 billion baht in net cash flow from operations and paid investors 20.2 billion baht in dividends. Its two main competitors are True and Dtac, which have about 33.7 percent and 20.8 percent of the mobile market respectively.

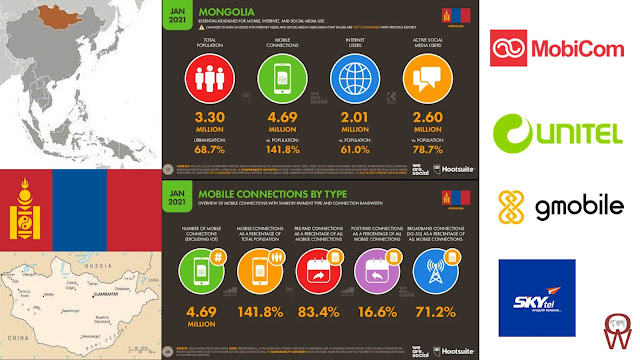

Mongolia has a population of 3.3 million but there are roughly 4.69 million mobiles, giving the penetration rate of 141.8%.

Telecommunications in Mongolia face unique challenges. It is the least densely populated country in the world and a significant portion of the population live a nomadic lifestyle. It has been difficult for many traditional information and communication technology (ICT) companies to make headway into Mongolian society. With almost half the population clustered in the capital of Ulaanbaatar, most landline technologies are deployed there. Wireless technologies have had greater success in rural areas.

Mobile phones are common, with provincial capitals all having 4G access. Wireless local loop is another technology that has helped Mongolia increase accessibility to telecommunications and bypass fixed-line infrastructure. For Internet, Mongolia relies on fiber optic communications with its Chinese and Russian neighbours.

There are four mobile operators in the country: MobiCom, Unitel, Skytel and G-Mobile.

Skytel and G-Mobile both only operate 3G networks in Ulaanbaatar and GSM-incompatible CDMA/EVDO networks in the rest of the country.

On MobiCom and Unitel 2G is on 900 and 1800 MHz, 3G (HDSPA) on 2100 MHz. 4G/LTE started in 2016 in Ulaanbaatar city only on 1800 MHz (Band 3) and new licenses were given out for 700 MHz (Band 28).

MobiCom is the biggest Mongolian cellular operator with 1.7 million active subscribers. It was established in 1996 as a joint Mongolian-Japanese venture and is the first Mongolian cell phone service. It was founded by Mongolian Newcom Group, and Japanese KDDI. As of 2015, Mobicom held over 1/3 of the market, with network coverage of 95% of the population.

Mobicom introduced 3G (HSPDA) networking in 2009. Its network support phones with 2100 MHz. 4G/LTE on 1800 MHz (Band 3) has been launched for all users without any surcharges and is enabled by default on all new SIM cards.

The operator has launched a 5G interoperability trial in partnership with its parent company and Telecom Infra Project (TIP).

Unitel (Universal or United telecommunications) was founded together with South Korea in 2005 as GSM mobile phone operator. In 2010 Unitel declared that it has become 100% indigenous company (i.e. Mongolian share owners bought all share from the Korean side).

Unitel network covers approximately 88% of population. In 2009 Unitel launched its 3G network on 2100 MHz. In 2016 they started 4G/LTE on 1800 MHz (Band 3) in the towns of Ulaanbaatar, Erdenet, Darkhan City, Dalanzadgad, Tsogttsetsii open for prepaid. It has a lower coverage, but better prices than MobiCom.

GSMA Intelligence estimated Unitel’s mobile connections at 1.6 million at end-Q3, placing it in the top two of four operators in Mongolia.

The operator has secured an option to be the first in the nation to employ satellite connectivity services from specialist Lynk Global. The company expects to be able to provide satellite services to standard mobile phones in 2022, when Unitel will have a “first-to-market right” to use it within the sprawling country.

In a statement, Unitel CEO Enkhbat Dorjpalam noted the topography, extreme weather and size of Mongolia meant it had very specialist coverage needs. The Unitel executive explained Mongolia was 1.6 million square kilometres with a population of 3.3 million spread across the country, adding “we have unique needs for coverage in our country given our nomadic lifestyle and extremely large livestock population of more than 70 million animals, which is a critical component to our society’s growth and resiliency.”

GMobile LLC was founded in April 2006. In 2008, GMobile was the first operator to introduce 3G technology in Mongolia and launched G-Internet phone service – mobile internet service based on 1X, EvDo technology. It presently only has175,000 subscribers.

Skytel Group has approximately 255,000 active subscribers the company's network functions on an HSPA+ network in Ulaanbaatar and [CDMA2000 1x] & [EVDO] network technology in the rest of the country.

Mongolia-based operator ONDO (IN Mobile Network LLC), is now the the fifth mobile operator in Mongolia, it has received a license to provide mobile services from the national telecommunications regulator Communications Regulatory Commission (CRC).

According to local media reports, ONDO is piloting the latest generation of high-speed mobile internet or 5G technology in Mongolia using cutting-edge technologies in the telecommunications industry.

The report said that ONDO plans to deploy 4G, 5G, and IoT networks, according to its new website, with an initial focus on the capital Ulaanbaatar.

Mongolia’s Communications Regulatory Commission (CRC) has awarded the country’s fifth mobile licence to ONDO (registered as IN Mobile Network), which plans to operate under the SuperNet brand. The firm plans to deploy 4G, 5G and IoT networks, according to its new website, with an initial focus on the capital Ulaanbaatar. A list of licensees published by the CRC shows IN Mobile Network’s concession expiring on 10 September 2031.

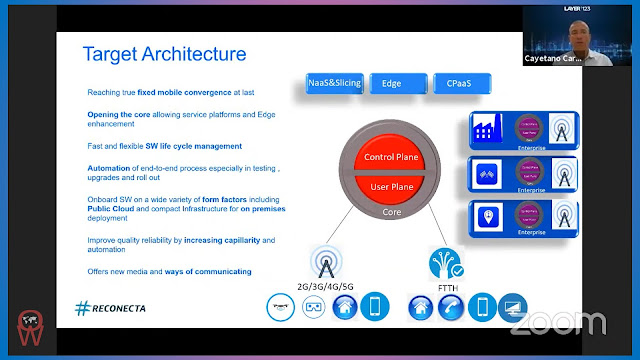

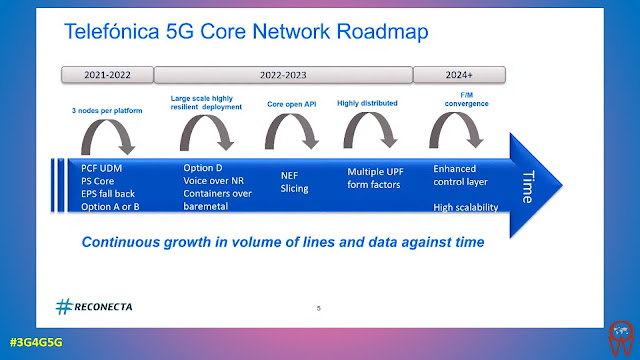

Many operators are working towards Fixed Mobile Convergence (FMC) to simplify their architecture and their operations. It was nice to hear Cayetano Carbajo, Director for Core, Transport and Service Platforms, GCTIO Telefónica SA at Layer 123 Conference. Kudos to them for sharing the video online (embedded below).

Like most other operators looking to bring the true 5G power to consumers and enterprises, Telefonica is moving to 5G Standalone architecture. It will be Cloud Native with Open Core Capabilities to develop application through API exposure.

As can be seen in the roadmap above, Slicing will allow QoS differentiation for different types of services. The most interesting thing is that Converged Core will allow signalling for 2G, 3G, 4G, 5G and for fixed line.

While this converged core will be containerised, there are some challenges today that they are expecting to be solved in the near future. The eventual reward is higher efficiency and a much higher level of automation.

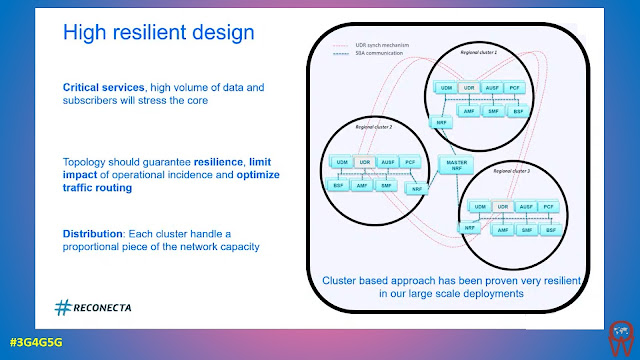

During the talk, Cayetano also discussed some technical 5G core details including their approach to increase resiliency. I highly recommend watching the embedded talk below. You may also find some of our other posts on related topics useful. They are highlighted below.

Back in April, the ICT ministry announced that the three major mobile carriers will share their 5G networks in remote coastal and farm towns in a move to accelerate the rollout of the latest generation networks. The Korea Herald reported:

The carriers -- SK Telecom Co., KT Corp. and LG Uplus Corp. -- signed an agreement so that 5G users can have access to the high-speed network regardless of the carrier they are subscribed to in 131 remote locations across the country, according to the Ministry of Science and ICT.

Under the plan, a 5G user would be able to use other carrier networks in such regions that are not serviced by his or her carrier.

The ministry said telecom operators will test the network sharing system before the end of this year and aim for complete commercialization in phases by 2024.

The ministry said the selected remote regions are sparsely populated, with a population density of 92 people per square kilometer, compared with those without network sharing at 3,490 people per square kilometer.

The move comes as the country races to establish nationwide 5G coverage, with network equipment currently installed in major cities.

South Korea's MNOs will power up its joint rural 5G network 25 November. The present 5G coverage (here KT) was realised without sharing. KT used 67,000 sites & 130,000 base stations to reach the 5G coverage shown in the map. Interesting to see how the rural network changes this. pic.twitter.com/niHPTZuLoR

In another article back in September, The Korea Herald reported:

The number of 5G network base stations in South Korea accounted for just 11 percent of the total in the second quarter, data showed Monday, amid continued user complaints against the latest generation networks.

As of the April-June period, there were 162,099 5G base stations in the country, compared with a total of 1.47 million mobile network base stations, according to data from the Korea Communications Agency.

The number of 5G base stations was far outnumbered by around 1 million 4G base stations and over 300,000 3G base stations.

In comparison, the number of 5G users accounted for 23.8 percent of the total in July at just over 17 million, while there were 50.5 million 4G users and 20.2 million 3G users.

The latest data comes as local mobile carriers have faced complaints from 5G users over spotty connection and slower-than-expected speeds since the networks' launch in April 2019.

At a recent GSMA conference, Daehun Lim, Head of Global Strategic Partnerships, LG Uplus shared the 5G Rural Network Sharing plans in more details. The picture on the top shows the timelines and the areas that are planned to be covered by each operator.

The network sharing will be based on MOCN which we have explained in our tutorial here.

Since the 5G spectrum allocation for all the operators is very similar, we don't expect any issues with the network sharing plan going forward. We will have to wait a couple of years before is becomes commercially available though.

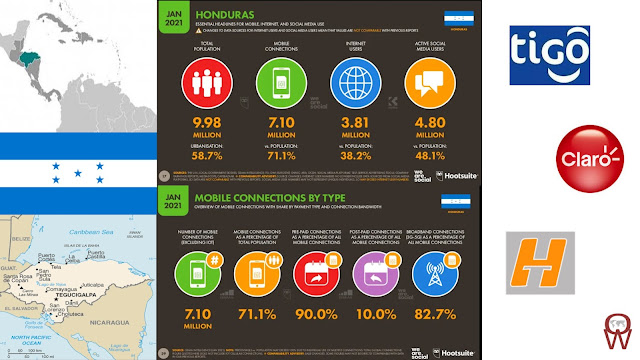

Honduras is one of the poorest countries in Central America and has long been plagued by an unstable political framework which has rendered telecom sector reform difficult. This has created real difficulties for operators as well as consumers. While the population is just under 10 million, it is as large as the size of England or the state of Pennsylvania in USA.

Fixed-line teledensity, at only 4.9%, is significantly lower than the Latin American and Caribbean average. Poor fixed-line infrastructure has been exacerbated by low investment and topographical difficulties which have made investment in rural areas unattractive or uneconomical. Consequently, the internet has been slow to develop. DSL and cable modem technologies are available but are relatively expensive and thus take-up has been low thus far, while higher speed services are largely restricted to the major urban centres. Nevertheless, the demand for broadband is steadily increasing and there has been some investment in network upgrades to fibre-based infrastructure. The government also provides free internet to around 75,000 households in Honduras.

On the positive side, these factors have encouraged consumer take-up of mobile services, a sector where there is lively competition supported by international investment. Even so, mobile penetration is substantially below the regional average. Revenue growth from the mobile sector looks promising in coming years as operators invest in their networks, expand their reach and upgrade their capabilities to accommodate mobile broadband services. Mobile data as a proportion of overall mobile revenue has increased steadily, though low-end SMS services will continue to account for the bulk of data revenue for some years.

There are 3 network providers in the Central American state of Honduras: Tigo (by Millicom), Claro (by América Móvil) and Honducel (by Hondutel). The three networks use different frequencies: Tigo's 2G and 3G is on 850 MHz, Claro's is on 1900 MHz and Honducel's is on 1800 MHz. In 2014/5 Tigo and Claro both started with 4G/LTE on the 1700 MHz (AWS Band 4) frequency.

Tigo is the clear market leader in the country with a solid 60% share, followed by Claro with 39% and Honducel with below 1%. Overall, 99% of municipalities in Honduras have 2G coverage and 49% have 3G coverage by any provider. So don't expect high speeds and data use especially in remote areas is still very slow. 4G/LTE started in 2014 in Tegucigalpa, San Pedro Sula and La Ceiba. For its license, Tigo is required to establish a 4G/LTE network in all major cities equivalent to around 15% of the country’s territory.

Honduras’s National Telecommunications Commission (Comision Nacional de Telecomunicaciones, Conatel) has indicated that it is poised to free up the 3.5GHz band for mobile use, as it seeks to ‘deliver the benefits of regional harmonisation with other Latin American countries.’ In freeing up the band, the regulator has identified international roaming, spectrum optimisation, investment cost and implementation time as its key priorities.

Spectrum in the 3.3GHz-3.7GHz range will be designated for mobile use, while frequencies in the 3.7GHz-3.8GHz range will be earmarked for fixed-wireless broadband use. The spectrum will be auctioned via a public tender, although no date has been disclosed.

Millicom’s Tigo brand is the largest mobile provider in Honduras. Millicom have revealed plans to spend $135 million on network improvements across three markets in Latin America, signing up with Ericsson to install LTE and 5G-ready kit to improve and expand coverage. The modernisation of its networks in Honduras, Paraguay and Bolivia is designed to widen its coverage to an additional 2.5 million people across 712 municipalities. Improvements include replacement of existing 4G packet core technology with an Ericsson dual-mode 5G core. Following the upgrade the operator will be able to use carrier aggregation technology.

The project is expected to take between two and three years to complete.

Claro by Mexican América Movil is the only viable competitor to Tigo in the country. It has a slightly lower coverage, but lower rates too. Claro’s 4G/LTE network started in 2015 and was initially made available in major cities such as Tegucigalpa, San Pedro Sula and La Ceiba.

Honducel was established in 2013 as mobile branch of the state-owned telecom operator Empresa Hondurena de Telecomunicaciones (Hondutel). Generally because of almost non-existent 3G coverage and unreliable service, it can't be recommended for travellers. It hardly reaches 1% market share and survives as their state-owned parent company still controls the landline market. In 2017 Honducel, has reportedly suffered heavy subscriber losses and ended the year below 10,000 mobile subscribers.

The Honduran government is said to be preparing a financial rescue package for state-backed telco Hondutel, as the scale of the company’s debt has been revealed. According to La Prensa, the stricken telco’s losses exceeded HNL298.9 million (USD12.4 million) in 1H21, which follows three consecutive years in which the company posted an annual net loss. Compounding the situation, state utility firm Empresa Energia Honduras (EEH) has cut off Hondutel’s electricity supply over the non-payment of its HNL450 million bill.

The government has indicated that the plan will see Hondutel modernised to become a gigabit-capable ‘broadband institution’. The tentative plans will see the government invest in a new submarine cable to double or triple the country’s available bandwidth. Despite the dire situation, the privatisation of the company has been ruled out, however.

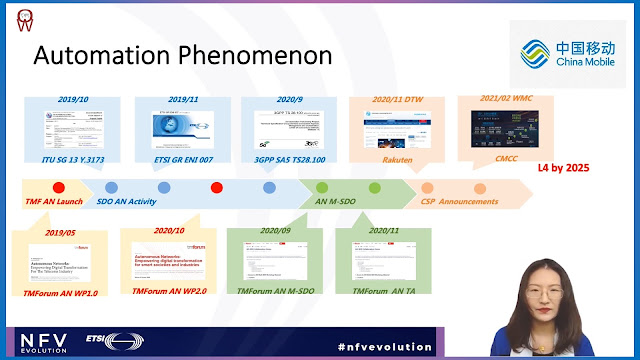

At the ETSI NFV Event back in April, Dr. Lingli Deng, China Mobile presented a talk on "From Orchestration Towards Automation". The abstract of the talk says:

Autonomous network proposes to optimize user experience, automate management operations, and maximize resource efficiency by simplifying network architecture, encapsulating autonomous domains, and providing closed loops for business/network operation control, and clarifies the target architecture and implementation path for network intelligence.

The autonomous network puts forward two dimensions of space and time requirements for the network management system of telecom operators:

On the one hand, the hierarchical, domain, and closed-loop autonomous architecture and cross-layer business-driven interaction of autonomous driving networks require operator network management systems to achieve functional enhancements ("addition") and interface simplification ("subtraction") in the spatial dimension.

On the other hand, the introduction of AI technology in autonomous driving networks and the complexity of network management itself require operators to achieve continuous iteration and gradual improvement in the time dimension of their network management system ("spiral upward").

In this speech, we will share China Mobile's autonomous network goals, approach, related practice, and overall thinking about the obstacles we are facing and proposed way forward, especially from the perspective of industrial collaboration, and the progress and next steps of ETSI NFV related work.

In particular, as an essential part of network management plane, MANO will need to be enhanced not only with simplified intent/policy interfaces, but also providing basis for enabling a complete zero-touch close loop (including VNF configuration), as well as the DevOps mechanism for AI models and/or analytics microservices embedded with network elements

The talk is embedded below:

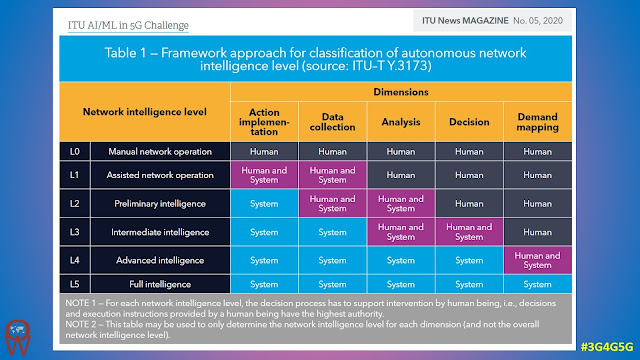

In the ITU News MAGAZINE last year, researchers from China Mobile Research Institute contributed an article on "A standards round-up on autonomous networks". The article provides a detailed list of specifications in various groups including ITU, 3GPP, ETSI, etc.

Quoting from the magazine:

There are discussions among standards development organizations (SDOs) about the level of autonomous capabilities in networks

The study of autonomous network levels (ANL) can provide reference and guidance to operators, vendors and other participants of the telecommunication industry for autonomous networks, standardization works and roadmap planning.

Since industrial convergence is the key for reducing the cost for any single vendor or single network operator, building an open collaboration platform for cohesively developing both a reference implementation for case-agnostic functional architecture and standardized external or internal interfaces would be the easy way for communication service providers (CSPs) to kick off and stay in the converged direction towards network autonomy.

For example, a rule-based policy engine could be one of the common functional modules to support both timed control tasks in Level 1, imperative closed loops in Level 2, and adding intent-to-rule translation modules in Levels 3 and 4.

The article starts on page number 23. You can download from here.

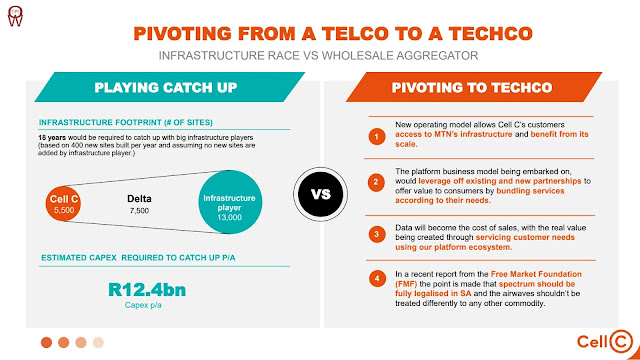

If you can't beat them, join them says the old proverb. The South African MNO Cell C has taken this seriously. A news article back in September said:

In a bid to give its customers access to world-class network quality, excellent service and innovative value offers, Cell C has over the last eight months deactivated 39% of its physical radio access network (RAN) towers with 100% migration in the Eastern Cape, Free State, Northern Cape and Limpopo.

Over the next four months, Cell C plans to decommission a further 5% of its towers, with a focus on parts of Kwa-Zulu Natal and Mpumalanga.

Rather than spending billions building network infrastructure to compete with its fellow mobile giants, the company concluded roaming agreements with network partners like MTN and Vodacom to use the spare capacity that they have on their networks.

Prepaid customers will roam on the MTN network, whilst post-paid customers will be on the Vodacom network.

We see a dual approach by Cell C here. Rather than putting all their eggs in a single basket, they have spread their risk portfolio.

In our blog post last year, we saw that both MTN and Vodacom has similar coverage and capabilities. This would mean that Cell C subscribers will win regardless of whichever network they are on.

With Vodacom, it looks like Cell C is using a roaming agreement and will act like a Thick MVNO. We have explained the different types of MVNOs here but if you prefer to watch a video then see here.

The approach with MTN, based on the above slide shared by them seems to be a combination of MVNO and MORAN. To understand what MORAN is, read here or watch the video here. Cell C explained it as follows back in June:

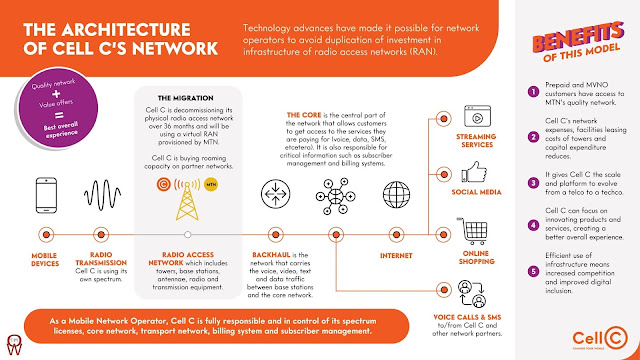

Cell C has successfully decommissioned 34 percent of its physical Radio Access Network (RAN) sites, while seamlessly migrating prepaid and Mobile Virtual Network Operator (MVNO) customers to roam solely on its partner network, MTN, via a virtual RAN.

The initial Cell C and MTN roaming agreement from 2018 provided coverage in areas outside of the main metros. The decommissioning of sites in these provinces means that where Cell C customers previously moved between Cell C and MTN towers, they will now only roam on MTN’s network through the virtual radio network provisioned for Cell C, which has wide network coverage.

Based on technology advances it is possible for network operators to avoid duplication of investment in RAN infrastructure. In this model, Cell C will decommission its physical RAN, which includes towers, base stations, antennae, radio and transmission equipment, while MTN will provision a virtual RAN. Cell C will use its own spectrum on this virtual RAN and manage the customer experience. As a mobile network operator Cell C is still responsible for its spectrum licenses, core network, transport network, billing system and subscriber management.

While Cell C continues to refer to the arrangement as 'virtual RAN', it shouldn't be confused with vRAN / Open RAN. It would be interesting to see how this arrangement works and if this will continue for 5G going forward.

Cell C's FY 2020 annual results presentation slides and video may be worth a watch.

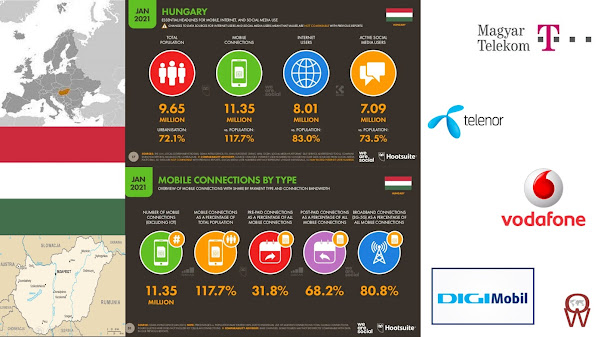

Hungary has the advantage of a developed telecom infrastructure, with a focus among operators to develop the 5G sector and upgrade fixed networks to provide a 1Gb/s service. Services based on 5G have been supported by the January 2021 multi-spectrum auction for spectrum in the 900MHz and 1800MHz bands. Digi Mobile failed to secure spectrum, which prompted the operator’s parent company to sell the unit to 4iG.

As in many other markets in the region, the number of fixed-lines continues to fall as subscribers migrate to the mobile platform for voice and data services. Operators have thus looked to bundled packages to boost revenue and retain subscribers. This strategy encouraged Vodafone Group to acquire UPC Hungary in mid-2019.

The dynamic mobile market is served by four MNOs and a small number of MVNOs. Mobile penetration is relatively high for the region, and there remains considerable growth in mobile broadband services delivered via upgraded networks. Revenue growth is focused on mobile data as operators struggle with competition and regulated tariff reductions.

Maygar Telekom is at the forefront of 5G developments, supported by the government, universities, other telcos and vendors forming the Hungarian 5G Coalition. By March 2021, Vodafone Hungary managed about 300 5G base stations in Budapest and its surrounds, as well as in a number of other cities.

The four mobile operators in Hungary are: Magyar Telekom (a.k.a Telekom, formerly T-Mobile/Westel), Telenor Hungary (formerly Pannon, partly state-owned), Vodafone Hungary and DIGIMobil (limited coverage, postpaid only)]

For the three major providers Telekom, Telenor and Vodafone 2G is on 900 and 1800 MHz, 3G is on 900 and 2100 MHz, while Digi works only on 1800 MHz with 2G/4G. The big three carriers are offering 4G/LTE services since 2015 on 800, 1800 and partly 2100, 2600 MHz (bands 1, 3, 7 and 20). LTE-A is available by big three providers in bigger cities in up to 300 Mbit/s. Telekom and Telenor have network sharing agreement for 4G on 800 MHz (B20) outside of Budapest and have therefore almost the same coverage on 4G/LTE. Generally Hungary has a quite good coverage with 4G/LTE networks and high speeds in most areas except Digi.

According to the recent Opensignal report on operators in Hungary, it was found that Telekom is the dominant operator when it comes to national mobile network experience. The operator won five out of the seven awards outright — Video Experience, Games Experience, Voice App Experience, Upload Speed Experience, and 4G Coverage Experience — and further jointly won the Download Speed Experience award with Telenor. It was noteworthy that Telekom users saw strong results for the experiential metrics — Excellent rating in Video Experience, Good ratings on Games Experience, and Voice App Experience. Telekom also had a considerable lead in Upload Speed Experience, with the users on its network observing 18.9% to 306.5% faster speeds compared to their peers. However, this was not the case for other metrics, as Telenor came close to challenge Telekom on most of them.

Hungary has held a strong position globally when it comes to mobile network experience and is striving to establish the same level of global success in the 5G era. The country opened its doors to 5G earlier last year with the auction of 5G capable bands in which three national operators — Telekom, Telenor, and Vodafone — acquired three bands of which the 2.1 GHz and 3.6 GHz bands were ready to be used immediately, while the 700 MHz band was available for use from September 2020 onwards. Since then, 5G deployments have been evolving in the country.

In terms of commercial 5G service, Vodafone claimed to be the first to launch services covering downtown Budapest in late 2019, using its existing 3500 MHz band frequencies. Telekom has claimed to have expanded 5G mobile services using the 2100 MHz band, via Dynamic Spectrum Sharing (DSS) technology and launched its commercial 5G network in April 2020 using the 3600 MHz band in selected areas of downtown Budapest and central Zalaegerszeg. In contrast, Telenor is yet to launch commercial 5G services, while the newest mobile operator — DIGIMobil — did not acquire any spectrum from the 5G auctions. The measurements from 5G users contribute to the overall scores included in this report.

In the future, as Hungary’s operators continue to make strides for a nationwide rollout it will be interesting to see how the mobile network experience in the country shapes up.

In this report, Opensignal used real-world data to compare the experience of our users on the country’s four key national operators — DIGIMobil, Telekom, Telenor and Vodafone — for a period of 90 days starting October 1, 2020.

Magyar Telekom Nyrt., often simply called Telekom, is the largest Hungarian telecommunications company. The former monopolist is now a subsidiary of (German) Deutsche Telekom.

It has the best and fastest network according to Opensignal. 4G/LTE is available on 800, 1800 and 2600 MHz and covers 98% of the population coverage map in up to 150 Mbit/s.

Telekom launched its commercial 5G network in April 2020 with spectrum in the spectrum from the 3.5GHz band, connecting areas in downtown Budapest and county capital Zalaegerszeg, it also switched on 5G base stations in the Lake Balaton region in July 2020.

Magyar Telekom stated 5G services are live in four other county capitals Debrecen, Szeged, Kecskemet and Szombathely. There is also 5G connectivity in the town of Budaors and 21 settlements around Lake Balaton.

DSS technology enables spectrum to be shared between 4G and 5G to a millisecond, allowing operators to rely on spectrum they already possess.

Telenor in Hungary was sold by Telenor to the Czech PPF Group in 2018, and since 2019 25% of it is owned by the state. It has pretty good coverage throughout the country. Their 3G is on 900 and 2100 MHz up to 42 Mbit/s and their 4G/LTE is available on 800, 1800 and 2600 MHz covering 99% of the population up to 150 Mbit/s.

Vodafone is the smallest provider in Hungary what the number of customers is concerned. It covers about 98% of the population on 2G and 3G and about 95% on 4G.

For 3G your device should be capable of the 900 MHz frequency, because most of its 3G antennas are based on it up to 21 Mbit/s. 4G/LTE network started in 2015 on 800 MHz and now available on 1800 and additionally on 2100 and 2600 MHz available for prepaid users in up to 75 Mbit/s.

Vodafone has signed a cooperation agreement Huawei along with Hungary's East-West Intermodal Logistics and British telecommunications operator, in a joint effort to build Europe's first smart railway hub managed by a 5G private network to be empowered by Huawei.

Vodafone Hungary and Huawei's Hungary subsidiary will provide a 5G private network for the project. 5G technology will be used to remotely control fully automatic gantry cranes for intelligent loading and unloading operations. It will be able to handle 1 million standard containers per year after project completion in the first quarter of next year.

A 4th LTE license to Romanian-backed RCS & RDS company (brand name: 'DIGI') was given out in 2014. They started their own 2G and 4G network on 1800 MHz (band 3) in May 2019.

Their coverage is very limited and there is no domestic roaming on other networks. They sell only postpaid packets.